The recent discussion about reclassifying marijuana under Schedule III controlled substance has sparked a lot of confusion—especially around one big question: Will insurance now cover cannabis cards or medical marijuana?

Short answer: No (at least not yet).

Long answer: It’s complicated, and worth understanding if you’re in the cannabis, healthcare, or packaging space.

In the United States, drugs are classified under the Controlled Substances Act into five schedules. Moving marijuana from Schedule I (where it currently sits alongside drugs like heroin) to Schedule III would:

Other Schedule III drugs include things like certain anabolic steroids and ketamine.

👉 This is a huge shift legally, but it doesn’t automatically change everything overnight.

Even if marijuana becomes Schedule III, health insurance is very unlikely to cover cannabis or cannabis cards immediately.

Insurance companies typically only cover drugs approved by the U.S. Food and Drug Administration.

👉 Exception: Some cannabis-derived drugs like Epidiolex are covered because they went through FDA approval.

A cannabis card is essentially a state-level authorization, not a formal prescription.

Even with Schedule III:

This inconsistency makes insurers cautious.

Insurance systems rely on:

Cannabis still lacks:

That makes it hard for insurers to price and approve coverage.

Rescheduling to Schedule III does open doors:

If cannabis-based medications follow the same path as Epidiolex, then insurance coverage becomes much more realistic.

For now, patients should expect:

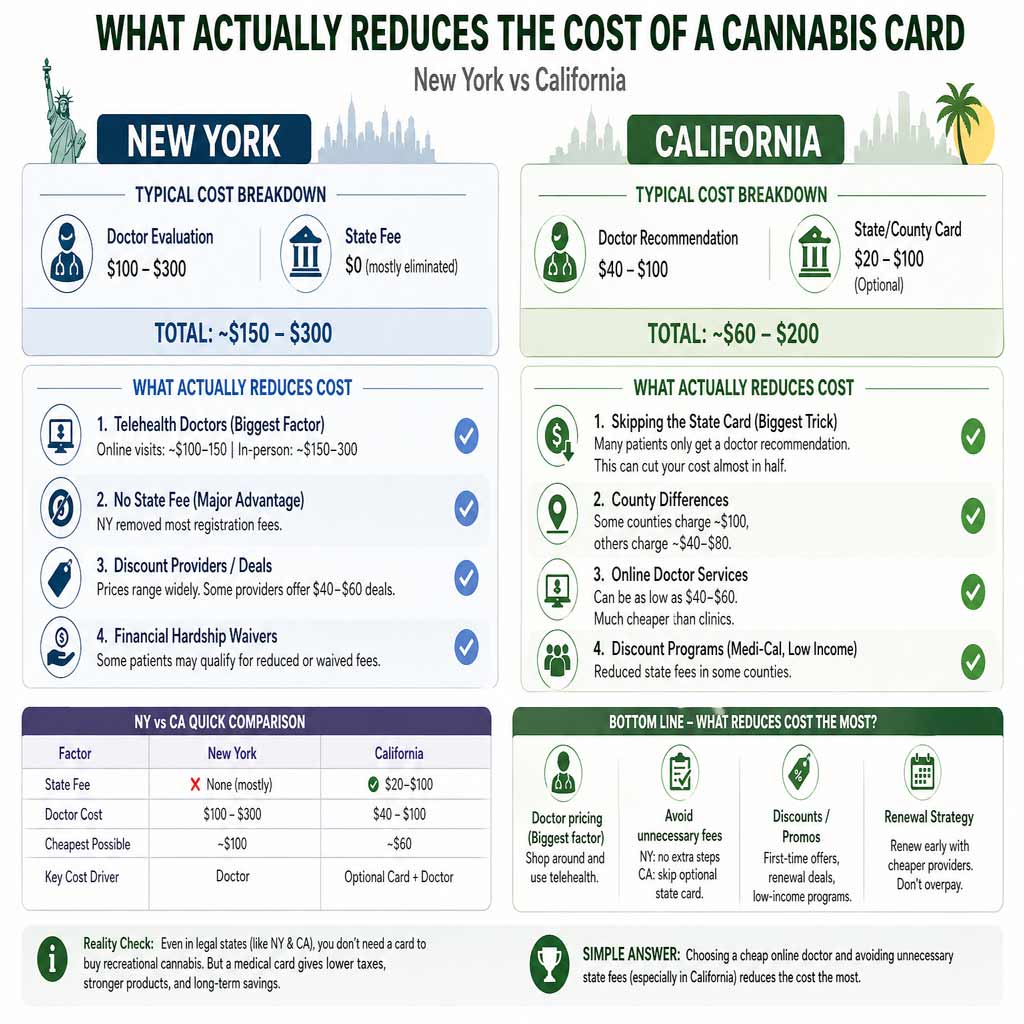

If you mean a medical cannabis card (MMJ card), the cost isn’t fixed—it varies by state—but a few practical things can bring it down.

1. State fee discounts

Many states offer reduced application fees if you qualify for programs like:

These can cut the state fee significantly.

2. Cheaper doctor evaluations

You usually need a physician’s recommendation. Prices vary a lot:

Shopping around can save you a noticeable amount.

3. Renewal timing

Some states offer:

4. Local competition

If you’re in a state with many providers, prices drop because clinics compete. Rural or limited-access areas are usually more expensive.

5. Promotions & bundles

Some clinics offer:

The biggest cost factors are:

Everything else just slightly reduces those.

👉 This can cut your cost almost in half

👉 Where you apply matters a lot

“online apt for $39… county card $50–100”

👉 Cheapest route = online + skip extras

| Factor | New York | California |

|---|---|---|

| State Fee | ❌ None (mostly) | ✅ $20–100 |

| Doctor Cost | $100–300 | $40–100 |

| Cheapest Possible | ~$100 | ~$60 |

| Key Cost Driver | Doctor | Optional card + doctor |

Does Schedule III marijuana mean insurance covers cannabis cards?

👉 No.

Not right now.

While reclassification is a major legal and business milestone, insurance coverage depends on FDA approval, standardized medical use, and regulatory clarity—none of which fully exist yet.

Most Popular States

Approved in minutes

100% online evaluation

Same-day approval available

See 20+ conditions

Compassionate Use Program

Save up to 25% on taxes

No appointment needed

Fast online process

Telehealth available

Quick certification